Measuring poverty or the poverty of measurement in Argentina

An editorial published by The Washington Post the 3 of April of 2026[1] He described Javier Milei's administration as a "radical experiment" with concrete results. He highlighted the reduction of poverty from 53% to 28% and inflation from 200% to 33% annually by February 2026.

In this note, the CLACSO researcher, Jessica PlaThis shows the weakness of that data and how it hides a reality of impoverishment, decreased purchasing power, and increasing indebtedness among families in Argentina.

Measuring poverty or the poverty of measurement

Reflections on the current Argentine context

Jessica Lorena Pla[2]

Poverty measurement in Argentina is based on monetary criteria. The Basic Food Basket (CBA) is calculated to determine the "indigence line" (the minimum income to cover nutritional requirements). Spending on non-food goods and services is added to this to obtain the Total Basic Basket (CBT), which establishes the "poverty line." The "poverty rate" indicates the percentage of the population without sufficient family income to afford the CBT. The data comes primarily from the Permanent Household Survey (EPH) conducted by the National Institute of Statistics and Censuses (INDEC). However, It has recently been questioned whether this monetary indicator adequately reflects the reality of families.

A recent note (Salvia, 2026) criticizes the "light" presentation of the data on the drop in poverty to 28,2% in 2025 (INDEC, 2026), urging a rigorous public debate that questions the mechanisms of construction of the indicator and its capacity to measure the reality of people's lives.

The author identifies a key methodological problem: the variation in income reporting. Since the end of 2023, the Permanent Household Survey (EPH) has documented a steady increase in reported income, particularly income not derived from employment (such as government programs and transfers). This shift is attributed to modifications in the survey questionnaire, designed to more effectively capture these transfers. The poverty rate falls because income that was not previously counted is being recorded, without necessarily representing a real increase in available money. “in the pocket” or in families’ purchasing power. Second, the consumption basket is outdated: the basket used to draw the poverty line is based on obsolete consumption patterns (measured by the 2017–2018 National Household Expenditure Survey). This methodological structure fails to capture the increase in non-food costs resulting from the realignment (increase) of relative prices between 2024 and 2025, which increased the weight of essential services (housing, transportation, energy, communications) in the family budget. Consequently, Households that are statistically classified as "not poor" actually have less income to cover essential expenses other than food, which contradicts the optimism suggested by the decrease in the indicatedr.

Simplifying the data to "achieving or not achieving" a certain income threshold to be considered "poor" or "not poor" narrows the debate and prevents a deeper understanding of the population's living conditions. Questions that arise from a broader perspective include: How do families manage to "achieve" this set of goods and services to "avoid poverty"? How many people in the household work to achieve this? How many hours do those who do work? What other strategies do they employ?

To understand how families "achieve" the Total Basic Food Basket (CBT), it is necessary to look beyond labor income and analyze survival strategies such as the financialization of basic consumptionRecent reports from the Central Bank of the Argentine Republic (BCRA, 2025) indicate that debt has become a central input for the survival of large sectors of the population: it is estimated that families characterized as poor only cover 64,4% with their labor or non-labor income, while the remaining third constitutes a "debt gap" that prevents the statistical fall into extreme poverty, but generates opacity in the measurements of social progress by sustaining living standards through the absorption of debt.

Similarly, 2026 marks a turning point: repayment capacity has reached its limit, resulting in a delinquency rate that has reached its highest level in over twenty years. Default is particularly critical in personal loans and the Fintech sector, where delinquency exceeds 30% in some segments due to the depletion of revolving credit capacity to cover current expenses.

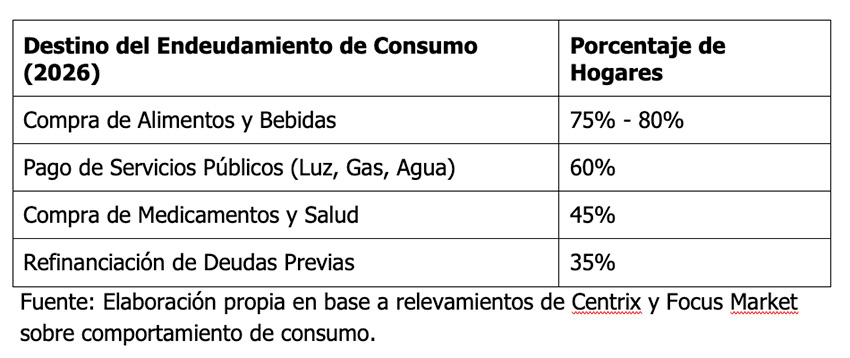

The main purpose of this debt is to cover basic needs, that is, those elements that are measured in the Poverty Basket:

This dynamic relies on credit that has mutated from a tool for durable goods to a bridge for subsistence: Between 75% and 80% of households go into debt to buy food, 60% for public services, and 45% for health..

This brief examination would lead us to suppose that the apparent stability of poverty indicators is, in reality, a symptom of a system that finances survival at the cost of a deprivation of the future, a pressure on daily life, and a limitation of future social mobility strategies within families.

A qualitative study on financial inclusion in Argentina, conducted between January and February 2026, reveals that debt among informal workers and low-wage earners is not an investment project, but rather a constant drain on resources for survival. Digital financing currently functions as a "funded social emergency" that absorbs the inflationary shock.

Even in formal employment, credit appears as the only answer to unforeseen events, quickly turning into a trap of installments. Roberto (50), a building manager, describes it:

"The first time was because our washing machine broke down... I checked the app and it said I had about seventy thousand pesos available... I took out what I needed. But then you realize the interest rates are high, that it's not worth it, but You might take it out because you ran short that month. You'll take another one out the following month.And then you have two loans running. And then three… and that's it. When you're facing the payments, you have nothing left to save. The salary arrives, it goes to expenses and installments, and that's it.... ".

For informal workers, the immediacy of Fintech platforms replaces traditional banking, serving as a "band-aid" for basic services:

"Mercado Pago is more convenient... it's for smaller expenses. For example, if my internet bill arrives on the 20th and I can't pay it, I take out a loan so they don't cut off my service. Or if I have to pay 60 and I only have 50 in cash, I order what I'm missing from Mercado«.

Given the opacity of the data—a product of changes in measurement instruments and the collection of income that does not reflect real purchasing power—the statistical dichotomy of being on one side or the other of the poverty line is insufficient to characterize the vulnerability of Argentine families. A comprehensive analysis must transcend the monetary threshold to capture critical dimensions where deprivation deepens: the gender gap, which disproportionately burdens caregiving in households with precarious survival strategies; territorial fragmentation, which conditions access to services and opportunities according to postal code, among other dimensions. Fundamentally, We must not lose sight of the generational crossroads we face.Macroeconomic management cannot hide behind improved aggregate indicators to mask these structural deficiencies. Subsistence debt as a temporary income band-aid is not a harmless phenomenon; it transfers precariousness to young people, who inherit a horizon of social mobility mortgaged by a lack of predictability and the accumulation of financial debt.

Discussing the construction of social indicators is, therefore, an intellectual and ethical imperative. Only a rigorous and informed public debate, one that recovers the perspective of social rights and quality of life, will allow us to design a collective development project that stops funding urgent needs at the expense of depriving future generations of their future..

References used

Central Bank of the Argentine Republic. (2025). Financial Inclusion Report: October 2025[PDF]. https://www.bcra.gob.ar/archivos/Pdfs/PublicacionesEstadisticas/Informe-inclusion-financiera-octubre-25.pdf

Focus Market. (May 15, 2026). 6 out of 10 households in Argentina have non-bank debtFocus Market Blog. https://focusmarket.com.ar/blog/6-de-cada-10-hogares-de-argentina-tiene-deuda-no-bancaria/

Informate Salta. (May 24, 2026). The new map of household debt in Argentina: how and why households are drowning. https://informatesalta.com.ar/economia/el-nuevo-mapa-del-endeudamiento-familiar-en-argentina–como-y-por-que-se-ahogan-los-hogares_a695d56f7583e69812801c53c

National Institute of Statistics and Censuses (INDEC). (2026). Incidence of poverty and extreme poverty in 31 urban agglomerations: Second half of 2025 (Technical Reports Vol. 10, No. 80; Living Conditions Vol. 10, No. 7). [PDF]. https://www.indec.gob.ar/uploads/informesdeprensa/eph_pobreza_03_269225CA3217.pdf

Messina, GM (2017). “The social construction of poverty indicators: an application to the case of Argentina.” Athenea Digital. Journal of Social Thought and Research, 17 https://doi.org/10.5565/rev/athenea.2045

First Edition. (May 23, 2026). Argentine economic crisis 2026: adjustment, poverty, delinquency and federalism. https://www.primeraedicion.com.ar/nota/101095339/crisis-economica-argentina-2026-ajuste-pobreza-morosidad-federalismo/

Salvia, A. (2026, March 23). The unbearable lightness of the poverty statistic. Profile. https://www.perfil.com/noticias/opinion/la-insoportable-levedad-del-dato-de-pobreza-por-agustin-salvia.phtml

[1] New data from Argentina shows the real answer to poverty.

[2] CONICET – CAECS Inter-American Open University. Director of the CLACSO Working Group “Inequalities and social change” (2026 – 2028).